Z-Score Revisited: Distress Signals in Business Valuation

Why Distress Signals Matter Before You Pick an Approach

Every business valuation engagement begins with two foundational questions: what is the appropriate standard of value, and what is the going-concern assumption? The second question is rarely stated explicitly, but it drives nearly every methodological choice that follows. A company valued as a going concern — using income or market approaches — will produce a fundamentally different conclusion than one valued on a liquidation premise. Getting that threshold question wrong is not a rounding error; it is a structural failure in the analysis.

The going-concern assumption requires the analyst to make a judgment about the subject company’s ability to continue operating for the foreseeable future. In litigation support engagements, that judgment is testable. Opposing counsel will test it. Courts will test it. The Altman Z-Score is one of the more useful tools for that testing — not because it is definitive, but because it is transparent, replicable, and defensible. It gives the analyst a structured, publicly documented framework that can be explained to a judge, a jury, and a rebuttal expert.

This article traces the original Z-Score model, its later variants for private companies and non-manufacturers, its practical role in a valuation engagement, and its limitations. For an interactive calculator, see the Altman Z-Score calculator on this site. For broader context on the original research, see Jeff’s 2013 QuickRead article, The Z-Score Revisited.

The Original 1968 Altman Model

Edward Altman published his discriminant analysis model in the Journal of Finance in 1968. The model was built on a sample of manufacturing firms and used five financial ratios to predict bankruptcy within two years. The ratios were selected for their collective predictive power, not simply because they were familiar.

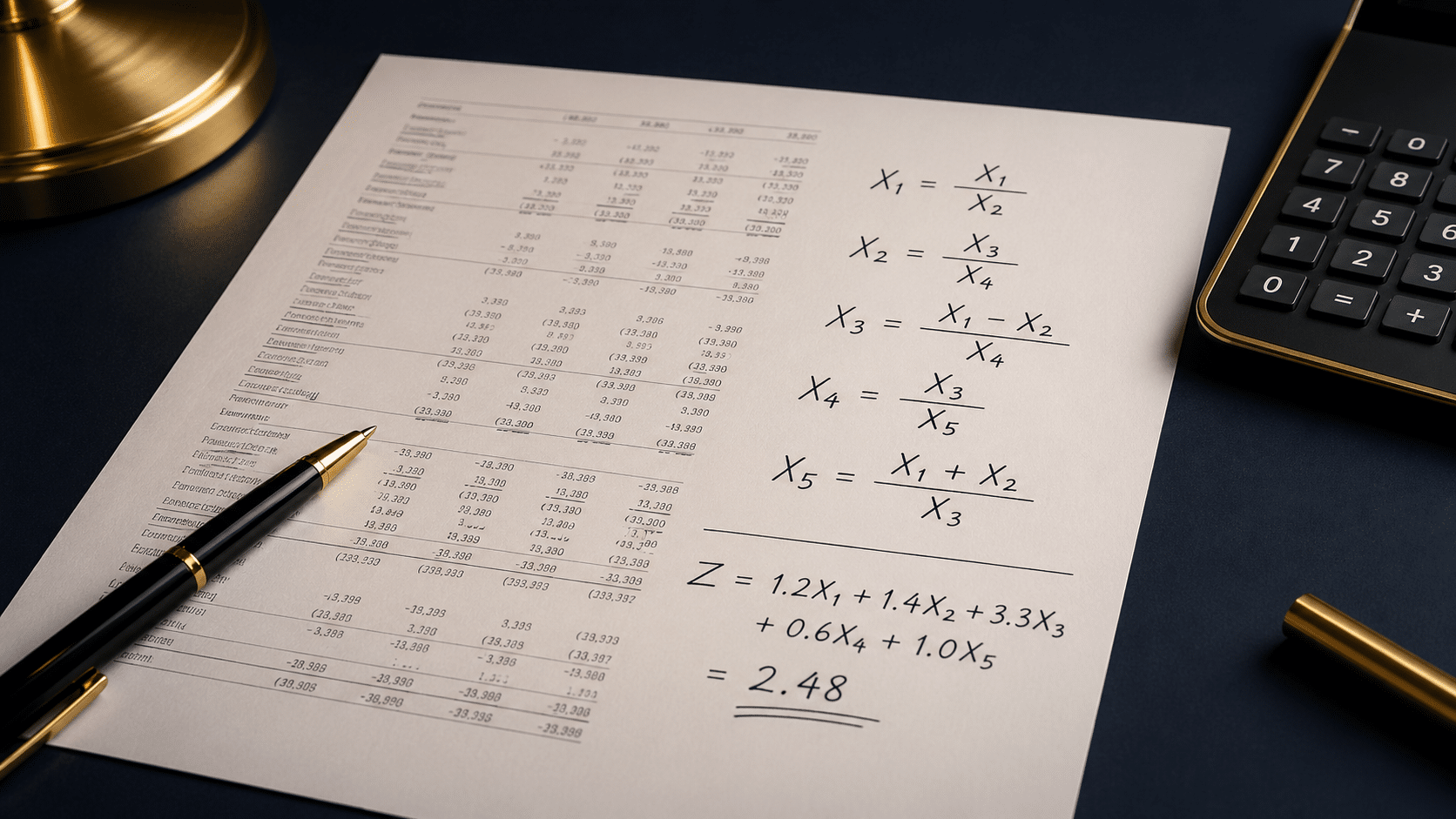

The five components are:

- X1 — Working Capital / Total Assets. A measure of short-term liquidity relative to asset base. Declining or negative working capital is often the first visible sign of operational stress.

- X2 — Retained Earnings / Total Assets. A proxy for accumulated profitability and the implicit age/reinvestment history of the firm. Young firms and firms with long histories of losses score poorly here regardless of current cash flow.

- X3 — EBIT / Total Assets. Return on assets based on operating earnings before interest and taxes. This ratio measures how effectively the asset base generates operating income independent of capital structure decisions.

- X4 — Market Value of Equity / Book Value of Total Liabilities. The original model used market value of equity, which is straightforward for publicly traded firms and requires a separate valuation step for closely held companies. This ratio represents the degree to which the firm’s equity cushion can absorb asset deterioration before liabilities exceed assets.

- X5 — Net Sales / Total Assets. Asset turnover. A measure of revenue efficiency relative to the asset base. Capital-intensive industries typically score lower here, which is one of the model’s known weaknesses.

The original model produces three zones:

| Z-Score | Zone | Interpretation |

|---|---|---|

| > 2.99 | Safe Zone | Low probability of financial distress within two years |

| 1.81 to 2.99 | Grey Zone | Indeterminate — heightened scrutiny warranted |

| < 1.81 | Distress Zone | High probability of financial distress within two years |

The grey zone is analytically important. A score in that range does not confirm distress; it signals that the going-concern assumption deserves explicit support in the report, not a perfunctory footnote. If your subject company scores between 1.81 and 2.99, the appropriate response is more analysis, not a conclusion either way.

Z’ and Z” — Variants for Closely Held Companies

Altman revised his model twice in subsequent decades to address the limitations of the original for companies outside the public-manufacturer sample.

Z’ — The Private Company Model

The Z’ model replaces the market value of equity in X4 with the book value of equity, making it applicable to closely held firms where a market price is not observable without a separate valuation. The coefficients and thresholds shift accordingly:

The substitution of book value for market value is a meaningful concession. Book equity is a lagging indicator; it captures historical accumulated equity but not the going-forward earning power that a market price embeds. In practice, for a closely held company already in financial difficulty, book equity is frequently overstated (asset write-downs are often deferred), which means the Z’ model may understate distress in precisely the cases where the measurement matters most. The analyst should note this limitation explicitly.

Z” — Non-Manufacturer Model

The Z” model removes the asset-turnover ratio (X5) entirely and recalibrates the remaining four components for use with service, retail, and other non-manufacturing firms. The X5 ratio systematically disadvantages asset-light businesses and would produce misleading scores if applied to a technology firm, a consulting practice, or most professional services entities.

For most closely held operating companies that are not publicly traded manufacturers, the Z” model is the appropriate starting point. Selecting the correct variant is not a minor technical detail — using the original model on a service company will produce a structurally biased result, and that bias will flow through to whatever conclusions the analyst draws about the going-concern assumption.

Practical Application in a Valuation Engagement

The Z-Score belongs in the analytical workpapers of virtually every business valuation engagement involving a company with meaningful debt or a recent history of operating losses. Here is how it fits into practice:

Going-Concern Testing

The primary use is going-concern testing. Before committing to an income or market approach, the analyst should run the appropriate Z-Score model against the most recent one to three years of financial statements. A stable safe-zone score over multiple periods supports the going-concern assumption. A declining trend — even if the most recent score remains in the safe zone — is worth noting. A grey-zone or distress-zone score requires explicit discussion in the report.

In a litigation context, an undisclosed distress-zone score is a cross-examination problem. If opposing counsel has access to the financial statements, they can run the model themselves. The analyst who did not address it will spend deposition time explaining the omission rather than defending the methodology. Address it in the report and address it proactively.

Approach Selection

A distress-zone score does not automatically eliminate the income or market approaches. It raises the burden of proof. The analyst who applies a discounted cash flow model to a distress-zone company needs to document why the going-concern assumption is supportable despite the score — typically through evidence of committed financing, a credible restructuring plan, or a strategic transaction that changes the company’s capital structure. Absent that evidence, a liquidation approach or an orderly-liquidation premise may be the more defensible choice.

For a broader discussion of approach selection in valuation engagements, see the business valuation services page.

Discount Rate Support

The Z-Score also informs the risk premium discussion in a build-up or CAPM rate development. A grey-zone or distress-zone company carries company-specific risk that should be reflected in the discount rate. The Z-Score provides an objective, documented basis for that adjustment — which is more defensible than a qualitative statement that “the company faces financial uncertainty.”

Limitations

The Z-Score is a useful tool, not a definitive answer. The analyst who presents it as the latter will lose credibility quickly. The material limitations are:

- Industry-specific distortions. Capital intensity, working-capital cycles, and sales-to-assets ratios vary enormously across industries. A capital-intensive manufacturer and a technology firm with few tangible assets will score very differently even if their financial health is equivalent. The analyst should contextualize the score against industry norms, not just the absolute thresholds.

- Off-balance-sheet obligations. Operating leases (particularly pre-ASC 842), contingent liabilities, unfunded pension obligations, and recourse debt that does not appear on the face of the balance sheet are invisible to the Z-Score. A company with a technically safe-zone score may have substantial off-balance-sheet leverage that the model does not capture.

- Financial engineering and accounting choices. Aggressive revenue recognition, deferred maintenance that understates expenses, and related-party transactions that distort working capital can all inflate the score. The analyst should normalize the financials before running the model, applying the same normalization adjustments used in the income approach.

- Look-back bias. The model was calibrated on historical data from a specific sample and time period. Its thresholds have not been formally recalibrated for current capital markets, interest rate environments, or post-financial-crisis accounting standards. The zones are indicative, not actuarial.

- Single-period snapshot risk. A single year’s Z-Score tells you less than a three-year trend. A company recovering from a temporary disruption may score in the grey zone in year one and the safe zone in years two and three. The analyst should compute the score for each available period and discuss the trajectory.

When to Escalate to Deeper Distress Analysis

The Z-Score is a screening tool. When it flags a concern, the appropriate response is to escalate, not to stop. Deeper analysis may include:

- Covenant compliance review — whether the company is in technical default on any debt instruments

- Liquidity stress testing — projected cash flows under base, downside, and severe-downside scenarios

- Capital structure analysis — weighted average cost of capital under distressed conditions, with attention to debt capacity and refinancing risk

- Management representation letters and audit opinion language — qualified or going-concern opinions from the auditor are independently significant

- Industry-specific distress benchmarks — sector-specific models exist for banking, retail, and emerging-market firms, among others

The Z-Score gets you to the right question. The deeper analysis answers it. For engagements where the going-concern assumption is genuinely in dispute, that deeper analysis should be documented in the workpapers and summarized in the report. The About Jeff page describes the credentials and professional standards — NACVA, SSVS No. 1 — that govern this type of engagement. For questions about a specific matter, the right next step is a direct conversation.

Try the interactive calculator.

Run the Z-Score on your own financial data using the Altman Z-Score calculator on this site. The tool supports the original, Z’, and Z” models with automatic zone classification.

Altman, E.I. (1968). “Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy.” Journal of Finance, 23(4), 589-609.

Harwell, J.H. (2013). “The Z-Score Revisited.” NACVA QuickRead, October 29, 2013. Practical application of the Z-Score for closely held company valuation.

For more on valuation methodology, see Insights and Business Valuation services.